.jpg)

According to the Deagel forecast, America’s population would plummet from just over 310 million in 2017 down to just 99 million in the near future. Western European nations, especially the U.K. and Germany, were forecast to see similarly drastic decreases in population, as were Canada and Australia.

If the Deagel calculations turn out to be even close to accurate, the most unsafe places to live over the next three years will be the United States, Canada and the U.K., followed by Germany, Australia and the rest of the E.U. nations. This population forecast was so controversial, showing population reductions of 68.5 percent in the United States (from 2017 levels) and between 25 and 70 percent for almost every Western European country, that the study mysteriously disappeared from Deagel’s website in March 2021.

But not all areas of the world will continue to decline. Some will actually have larger populations in the near future, according to the Deagel forecast. The safest places to be living would appear to be Central and South America, China and Africa. Interestingly, Russia came in as neutral, not gaining or losing population.

Is this Deagel forecast map a prediction of who will win a future World War III?

Or will a Global Pandemic or maybe a Vaccine be the reason for this!

Historically, a change in the economic paradigm

Deagel organization predicts massive global depopulation of 50 to 80%. Deagel.com

Deagel, a true intelligence organization for the US government, predicted a massive 50-80% global depopulation. Few people are familiar with this website and even more say the organization does not legitimately exist. Despite the overwhelming removal of its significance, WikiLeaks documents revealed that it was legitimately used as a reference material in a Stratfor report on the technological capabilities of the North People's Republic of Korea.

According to its own website, Deagel provides news and information on international military aviation and advanced technologies. The website contains articles from 2003, but little is known about the real owners. Many online researchers have mistakenly confused this site with "deagle.com" which is owned by Edwin A. Deagle, Jr., Assistant to the Secretary of Defense and Assistant Secretary of Defense.

Deagel's reports, particularly the aforementioned research on North Korea, were also provided to the president during presidential briefings. Deagel thus provides information which is then used by global intelligence communities and governments. Here is a partial list of known Deagel partners and customers, according to their own websites: National Security Agency, North Atlantic Treaty Organization (NATO), Organization for Economic Co-operation and Development (OECD), the Organization for Security and Cooperation in Europe (OSCE), the Russian Defense Procurement Agency, Stratfor, the World Bank and the United Nations.

The advantage of these forecasts is that the Deagel site has no conflict of interest in these forecasts. They are literally mercenaries. The site analyzes which budgets will be allocated to which markets to purchase military aircraft. That’s all that really matters to them. These forecasts are based on the reconciliation of various publicly available reports from institutions such as the CIA, the IMF and the UN. They also include a small amount of data from a variety of "dark sources" such as web gurus. But all of these sources are on the internet. The list is constantly evolving. Forecasts of population growth or decline, military spending, and purchasing power parity across countries around the world have fluctuated somewhat, but since 2015 one prediction has not changed: China will be the largest economy on the planet soon.

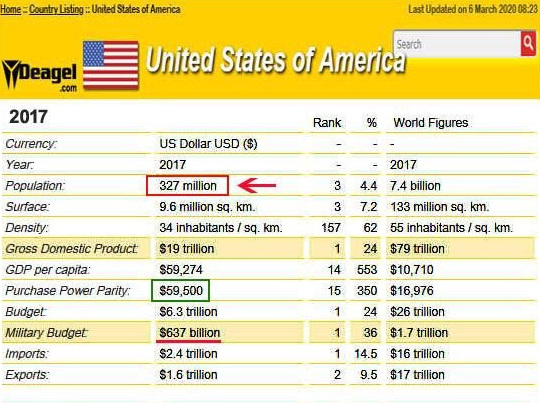

This highly regarded intelligence organization has bleak prospects for the United States in the years to come, including an 81% decline in its population, from 327 million in 2017 to 100 million. In fact, it predicted a similar cataclysmic fate for the UK, Australia, Germany, Japan, Denmark, and other US allies. For example, according to Deagel, the population of France will increase from 67 million inhabitants in 2017 to 39 million, that of England will increase from 66 million to 15 million, that of Australia from 23 million to 15 million. , that of Germany from 81 million to 28 million, while the population of Canada will fall from 36 million in 2017 to 26 million.

To make matters even stranger, a statement on Deagel's predictions page apparently claims that the population movements are due to suicide and assures us that the organization is not "a merchant of death or satanic worship":

“Historically, a shift in the economic paradigm has resulted in a death toll that is seldom highlighted by mainstream historians. When the transition from rural areas to large cities occurred in Europe, many people unable to accept the new paradigm committed suicide. They committed suicide by a psychological factor. This is not common but it is true. A new crisis combines old, well-known models with new ones. We are not a dealer in death or in satanic worship or in weapons as there are rumors floating around the Internet about this. "

“Take into account that the forecast is nothing more than a model, whether it is wrong or correct. It is not the word of God or some magical device that predicts the future. "- Deagel.com

Most of the economic and demographic data used to make the forecasts are widely available from institutions such as the CIA, IMF, UN, US government, etc.

There is a tiny fraction of the data coming from a variety of shadow sources such as internet gurus, unsigned reports and others. But all of these sources come from the Internet and are in the public domain for at least a minority. For example, several years ago, Dagong, the Chinese rating agency, published a report analyzing the physical economy of states by comparing it to that of China, Germany and Japan. The conclusion was that the US GDP was between $ 5,000 and $ 10,000 billion instead of $ 15 trillion, as the USG officially stated. We assume that official data, especially economic data, published by governments are false or distorted to some extent. Historically, it is well known that the former Soviet Union drew up false statistics years before its collapse. The West and other countries are now inventing their numbers to hide their real situation. We are sure that many people can find government statistics in their own country which, through their own personal experience, are hard to believe or are so optimistic that they may belong to another country.

Despite the "quantity" of digital data, there is a "quality" model that does not translate directly into digital data. The 2014 strain of Ebola has a death rate of 50-60%, but try to imagine what would happen if there was an Ebola pandemic with hundreds of thousands or millions of people infected with it. So far, the few cases of people infected with the Ebola virus have “benefited” from intensive health care with antiviral and respiratory assistance, but mostly with abundant human support from doctors and nurses. In a pandemic scenario, this type of health care will not be available for the overwhelming number of infected, leading to a dramatic increase in the death rate due to the lack of appropriate health care. The “quality” factor is that the death rate could increase by 80-90% in a pandemic scenario from the reported rate of 50-60%. The number itself does not matter what is relevant is the fact that the scenario may evolve beyond the initial conditions of a 50% balance sheet to over 90%. By the way, no pandemic or nuclear war is included in the forecast.

Economic Collapse Then Migration?

The key to understanding the process America will enter the next decade is migration. In the past, especially in the 20th century, the key factor that enabled the United States to achieve its status as a colossus was immigration with the benefits of population expansion favoring credit expansion and brain drain. the rest of the world for the benefit of States. The collapse of the Western financial system will wipe out the standard of living of its people while putting an end to ponzi schemes such as the stock market and pension funds. The population will be hit so hard by a full array of bubbles and ponzi schemes that the migration engine will start to work in reverse acceleration due to ripple effects, leading to the demise of states. This situation invisible to states will cascade with unprecedented and devastating effects on the economy. The offshoring of jobs will surely end with many American companies relocating abroad thus becoming foreign companies !!!!

We see a significant portion of the American population migrating to Latin America and Asia while migration to Europe - suffering from a similar illness - will not be relevant. Nonetheless, the death toll will be horrendous. Take into account that the population of the Soviet Union was poorer than Americans today or even then. The ex-Soviets suffered during the next struggle in the 1990s with a significant death toll and loss of national pride. Could we say "twice the pride, twice the fall"? Nope. America's standard of living is one of the highest, well over double that of the Soviets while adding a service economy that will accompany the financial system. When retirees see their retirement disappearing in front of their eyes and there are no service jobs, you can imagine what will happen next. At least young people can migrate. Never in human history have there been so many elders in the population. Over the past centuries, people have been fortunate enough to reach their 30s and 40s. America's downfall is expected to be much worse than that of the Soviet Union. A confluence of crisis with a devastating result.

The demographic crisis in the former Soviet Union countries extended for more than two decades, if we admit that it ended at the beginning of this decade (2010s). The demographic crisis will hit the world in the near future and is expected to last between three and eight decades more or less depending on technological advances and environmental issues. The consequence is more likely a frozen picture with the number of populations remaining the same for a very, very long period of time. Countries expect population figures to reflect births / deaths as well as migratory movements. Many countries will increase their gross populations as a result of immigration while their indigenous populations may decrease.

Over the past two thousand years we have seen Western civilization built around the Mediterranean Sea move to Northern Europe, then in the mid-twentieth century move to an Atlantic axis and finally focus on the United States. United for the past 30 years. The next step will see civilization centered on Asia with Russia and China at the top. Historically, a shift in the economic paradigm has resulted in a death toll that is seldom highlighted by mainstream historians. When the transition from rural areas to large cities occurred in Europe, many people unable to accept the new paradigm committed suicide. They committed suicide by a psychological factor. This is not common but it is true. A new crisis combines old, well-known models with new ones.

Sorry to disappoint many of you with our forecast. They have worsened more and more each year since the start of the pre-crisis in 2007. It is already said that this site is non-profit, built on free time and we provide our information and services AS IS without others. explanations and / or guarantees.

We are not tied to any government in any way. We are not a dealer in death or in satanic worship or in weapons as there are rumors floating around the Internet about this. Be aware that the forecast is nothing more than a model, whether it is wrong or correct. It is not the word of God or some magical device that predicts the future.

There are 179 countries listed with a forecast. Deagel Forecast For USA – Population Drops 70% Deagel.com is a global military intelligence site. They have had an online presence since 2003. They report on high-level military equipment assets and keep track of military expenditures by country “with nearly impeccable numbers”. Population In Millions, Real Gross Domestic Products In USD Billions, Defense Budget In USD Billions, Power Purchase Parity In USD |

2 India 1,341 $7,320 $110 $5,456

3 Russia 141 $6,177 $186 $43,557

4 Brazil 210 $3,241 $37 $15,412

5 Indonesia 267 $2,608 $14 $9,766

6 Japan 103 $2,431 $17 $23,593

7 Mexico 124 $1,711 $6.1 $13,724

8 United States of America 99 $1,630 $32 $16,374

9 Pakistan 218 $1,179 $26 $5,389

10 Iran 81 $1,174 $18 $14,325

11 Thailand 64 $1,126 $11 $17,333

12 Egypt 105 $1,107 $14 $10,514

13 Malaysia 33 $1,031 $10 $30,920

14 Nigeria 187 $1,012 $5 $5,406

15 Philippines 117 $960 $8.3 $8,207

16 Italy 43 $945 $12 $21,600

17 Turkey 71 $833 $9.8 $11,653

18 Saudi Arabia 25 $806 $36 $31,873

19 Colombia 49 $806 $18 $16,388

20 Netherlands 16 $797 $9.7 $47,451

21 South Korea 37 $775 $13 $20,902

22 France 39 $718 $10 $18,368

23 Vietnam 99 $669 $11 $6,762

24 Canada 26 $663 $6.4 $25,208

25 Taiwan 18 $647 $7.3 $34,942

26 Argentina 41 $640 $4.3 $15,621

27 Poland 33 $599 $6.1 $18,036

28 Bangladesh 178 $565 $4.5 $3,173

29 Iraq 33 $514 $21 $15,235

30 Romania 21 $484 $4.4 $23,041

31 Algeria 43 $483 $13 $11,078

32 Chile 18 $482 $7.9 $26,665

33 Germany 28 $413 $2.9 $14,704

34 South Africa 45 $400 $2.3 $8,725

35 Spain 27 $388 $2.1 $13,986

36 Peru 31 $386 $3 $12,101

37 Kazakhstan 18 $315 $1.9 $17,404

38 Czechia 9.9 $302 $2.1 $30,589

39 Morocco 33 $298 $7.1 $8,853

40 Australia 15 $280 $2.8 $18,441

41 Myanmar 58 $278 $5 $4,749

42 Venezuela 29 $267 $1.7 $9,132

43 Hungary 9.4 $258 $1.5 $27,587

44 Singapore 5 $252 $4.2 $50,863

45 Sri Lanka 22 $241 $3.7 $10,577

46 Ethiopia 100 $238 $1.3 $2,369

47 Finland 5.3 $215 $3.6 $40,857

48 Belgium 8.1 $207 $1.9 $25,767

49 Kenya 50 $180 $2.1 $3,595

50 Dominican Republic 11 $177 $0.7 $15,766

51 Portugal 8.1 $172 $2.2 $21,230

52 Sudan 40 $168 $2.8 $4,149

53 Austria 6.2 $167 $1.1 $26,908

54 Afghanistan 33 $165 $6.3 $4,924

55 Ukraine 31 $164 $2.4 $5,188

56 Uzbekistan 30 $164 $3.2 $5,389

57 Ecuador 15 $164 $2.7 $10,599

58 Azerbaijan 9.6 $158 $4.9 $16,456

59 Sweden 7.2 $157 $1.4 $21,958

60 Slovakia 5.1 $147 $1.1 $29,069

61 Switzerland 5.3 $144 $0.7 $27,124

62 United Kingdom 14 $131 $1.4 $9,068

63 Greece 8.1 $129 $2 $16,105

64 Bulgaria 6.1 $127 $1.2 $20,767

65 Angola 19 $125 $4.1 $6,437

66 United Arab Emirates 4.7 $124 $4.8 $26,651

67 Lebanon 6.6 $120 $3.3 $18,333

68 Oman 3.6 $119 $7.4 $33,011

69 Norway 3.8 $115 $1.5 $30,188

70 Guatemala 16 $112 $0.3 $6,630

71 Tanzania 42 $111 $0.8 $2,611

72 Cuba 10 $110 $3.2 $10,190

73 Cote d'Ivoire 25 $104 $1.1 $4,092

74 Ghana 27 $100 $0.3 $3,590

75 Denmark 3.8 $94 $1 $25,057

76 Cameroon 24 $94 $0.9 $3,872

77 Qatar 1.8 $91 $3.4 $51,731

78 Belarus 7.9 $86 $0.5 $10,968

79 Turkmenistan 5.6 $82 $1.5 $14,774

80 Bolivia 11 $82 $0.8 $6,846

81 Kuwait 2.4 $81 $2.9 $34,104

82 Nepal 33 $81 $0.8 $2,421

83 Panama 3.8 $79 $0.4 $20,694

84 Costa Rica 5.2 $78 $ $15,199

85 Tunisia 10 $77 $0.6 $7,258

86 Lithuania 2.7 $73 $0.6 $27,174

87 Croatia 3.8 $70 $0.7 $18,850

88 Cambodia 17 $69 $0.9 $3,998

89 Uganda 36 $68 $0.7 $1,877

90 Serbia 6 $63 $0.6 $10,717

91 Democratic Republic of Congo 81 $63 $0.7 $776

92 Jordan 6.9 $62 $1.6 $9,144

93 Paraguay 7.2 $62 $0.7 $8,679

94 Syria 16 $61 $4.4 $3,812

95 Yemen 27 $59 $1.3 $2,172

96 New Zealand 3.3 $48 $0.3 $14,711

97 Slovenia 1.7 $47 $0.4 $27,708

98 Israel 4 $46 $1.7 $11,798

99 Zambia 15 $44 $0.4 $2,886

100 Senegal 14 $44 $0.5 $3,066

101 Laos 7.7 $44 $0.1 $5,844

102 Latvia 1.8 $43 $0.4 $24,795

103 El Salvador 5.3 $42 $0.3 $7,965

104 Honduras 9.8 $42 $0.3 $4,282

105 Gabon 1.9 $41 $0.4 $21,794

106 Mali 16 $40 $0.5 $2,472

107 Burkina Faso 18 $40 $0.4 $2,209

108 Republic of the Congo 5.3 $37 $0.6 $7,128

109 Botswana 2.3 $36 $0.6 $16,155

110 Georgia 4.7 $36 $0.6 $7,770

111 Bosnia and Herzegovina 3.6 $35 $0.3 $9,756

112 Albania 2.8 $35 $0.3 $12,485

113 Rwanda 12 $33 $0.3 $2,572

114 Brunei Darussalam 0.4 $32 $0.6 $73,859

115 Mozambique 26 $31 $0.2 $1,229

116 Chad 12 $31 $0.5 $2,538

117 Uruguay 2.8 $30 $0.5 $10,761

118 Mongolia 3.1 $30 $0.2 $9,772

119 Madagascar 24 $28 $0.1 $1,139

120 Nicaragua 6.2 $27 $0.1 $4,466

121 North Macedonia 1.9 $27 $0.2 $14,380

122 Benin 10 $27 $0.2 $2,600

123 Tajikistan 9.2 $25 $0.2 $2,732

124 Papua New Guinea 7.6 $23 $0.1 $3,065

125 Mauritius 1.4 $23 $0 $17,566

126 Niger 17 $23 $0.4 $1,321

127 Jamaica 2.8 $21 $0.1 $7,612

128 Zimbabwe 14 $21 $0.3 $1,492

129 Estonia 0.9 $20 $0.4 $21,806

130 Namibia 2.3 $20 $0.5 $8,550

131 Armenia 2.9 $20 $0.5 $6,938

132 Bahrain 0.8 $17 $0.4 $20,778

133 Ireland 1.3 $16 $0 $12,355

134 Trinidad and Tobago 1 $16 $0.1 $16,041

135 Cyprus 0.8 $15 $0.2 $19,087

136 Equatorial Guinea 0.7 $15 $0 $22,236

137 Kyrgyzstan 5.8 $14 $0.1 $2,455

138 Mauritania 3.8 $14 $0.4 $3,715

139 Guinea 11 $13 $0.1 $1,137

140 Malawi 17 $13 $0.1 $789

141 Togo 7.5 $13 $0.2 $1,860

142 Libya 3.3 $11 $ $3,513

143 Montenegro 0.6 $11 $0.1 $18,861

144 Timor-Leste 1.4 $11 $0.2 $8,360

145 Haiti 9.4 $10 $ $1,152

146 Burundi 10 $9.9 $0.2 $941

147 Moldova 2.8 $9.5 $0 $3,463

148 Eswatini 1.4 $9.5 $0.1 $6,989

149 Sierra Leone 5.9 $8.2 $0 $1,390

150 Suriname 0.5 $7.4 $0 $13,621

151 Fiji 0.9 $7.1 $0.1 $7,847

152 Eritrea 6 $6.3 $0.2 $1,046

153 Guyana 0.7 $6.3 $0.1 $8,679

154 Malta 0.3 $6.2 $0 $21,156

155 Maldives 0.4 $6.2 $0.1 $15,824

156 Bhutan 0.8 $5.9 $ $7,515

157 Bahamas 0.3 $5 $ $18,312

158 Cape Verde 0.6 $4.4 $0 $7,725

159 Somalia 9.9 $4.3 $ $430

160 Central African Republic 6 $4.2 $0 $694

161 Djibouti 0.9 $4.1 $0.1 $4,653

162 Luxembourg 0.2 $3.9 $0 $19,402

163 Lesotho 1.7 $3.6 $0 $2,057

164 Guinea-Bissau 2 $3.6 $0.1 $1,821

165 Barbados 0.2 $3 $ $12,857

166 Iceland 0.2 $2.8 $0 $14,185

167 Belize 0.4 $2.7 $0 $7,671

168 Gambia 2 $2.6 $0 $1,303

169 Liberia 3.8 $2.4 $0 $627

170 Grenada 0.1 $1.9 $ $17,098

171 Comoros 0.9 $1.8 $0 $2,020

172 Solomon Islands 0.7 $1.8 $0 $2,734

173 Saint Lucia 0.1 $1.4 $ $10,978

174 Samoa 0.2 $1.4 $ $7,124

175 Saint Vincent and the Grenadines 0.1 $1.3 $ $12,884

176 Sao Tome and Principe 0.2 $0.8 $ $3,418

177 Tonga 0.1 $0.7 $ $6,645

178 Kiribati 0.1 $0.4 $ $3,483

179 Micronesia 0.1 $0.3 $ $3,282

Disclaimer*

In 2014 Deagel.com published a disclaimer about the forecast. Stating in six years the scenario had changed dramatically. This new disclaimer is meant to single out the situation from 2020 onwards. Talking about the United States and the European Union as separated entities no longer makes sense. Both are the Western block, keep printing money and will share the same fate.

After COVID we can draw two major conclusions:

- The Western world success model has been built over societies with no resilience that can barely withstand any hardship, even a low intensity one. It was assumed but we got the full confirmation beyond any doubt.

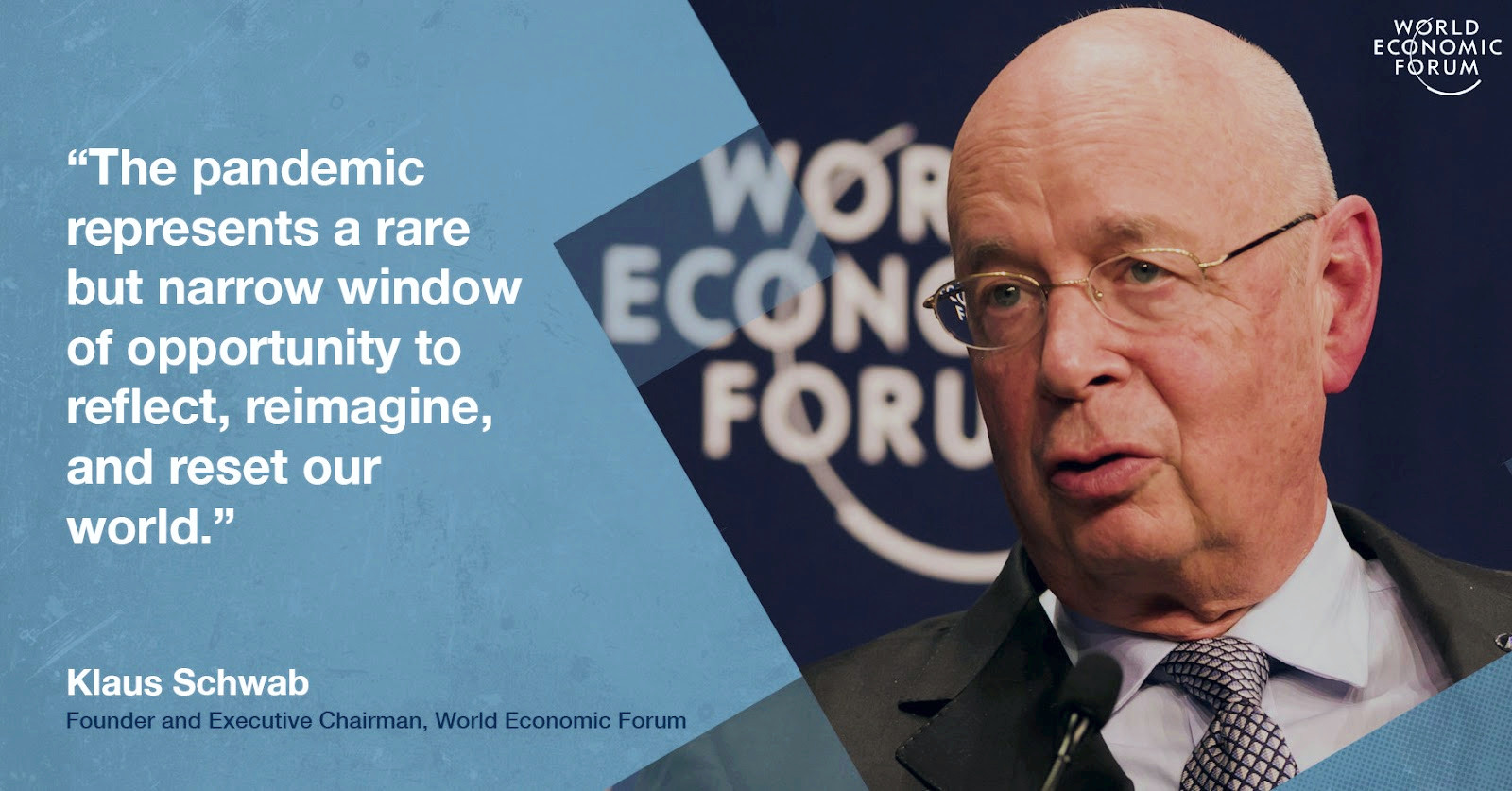

- The COVID crisis will be used to extend the life of this dying economic system through the so called Great Reset.

The Great Reset; like the climate change, extinction rebellion, planetary crisis, green revolution, shale oil (…) hoaxes promoted by the system; is another attempt to slow down dramatically the consumption of natural resources and therefore extend the lifetime of the current system. It can be effective for awhile but finally won’t address the bottom-line problem and will only delay the inevitable. The core ruling elites hope to stay in power which is in effect the only thing that really worries them.

The collapse of the Western financial system - and ultimately the Western civilization - has been the major driver in the forecast along with a confluence of crisis with a devastating outcome. As COVID has proven Western societies embracing multiculturalism and extreme liberalism are unable to deal with any real hardship. The Spanish flu one century ago represented the death of 40-50 million people. Today the world’s population is four times greater with air travel in full swing which is by definition a super spreader. The death casualties in today’s World would represent 160 to 200 million in relative terms but more likely 300-400 million taking into consideration the air travel factor that did not exist one century ago. So far, COVID death toll is roughly 1 million people. It is quite likely that the economic crisis due to the lockdowns will cause more deaths than the virus worldwide.

The Soviet system was less able to deliver goodies to the people than the Western one. Nevertheless Soviet society was more compact and resilient under an authoritarian regime. That in mind, the collapse of the Soviet system wiped out 10 percent of the population. The stark reality of diverse and multicultural Western societies is that a collapse will have a toll of 50 to 80 percent depending on several factors but in general terms the most diverse, multicultural, indebted and wealthy (highest standard of living) will suffer the highest toll. The only glue that keeps united such aberrant collage from falling apart is overconsumption with heavy doses of bottomless degeneracy disguised as virtue. Nevertheless the widespread censorship, hate laws and contradictory signals mean that even that glue is not working any more. Not everybody has to die migration can also play a positive role in this.

The formerly known as second and third world nations are an unknown at this point. Their fate will depend upon the decisions they take in the future. Western powers are not going to take over them as they did in the past because these countries won’t be able to control their own cities far less likely countries that are far away. If they remain tied to the former World Order they will go down along Western powers but won’t experience the brutal decline of the late because they are poorer and not diverse enough but rather quite homogenous used to deal with some sort of hardship but not precisely the one that is coming. If they switch to China they can get a chance to stabilize but will depend upon the management of their resources.

We expected this situation to unfold and actually is unfolding right now with the November election triggering a major bomb if Trump is re-elected. If Biden is elected there will very bad consequences as well. There is a lot of bad blood in the Western societies and the protests, demonstrations, rioting and looting are only the first symptoms of what is coming. However a new trend is taking place overshadowing this one.

The situation between the three great powers has changed dramatically. The only relevant achievement of the Western powers during the past decade has been the formation of a strategic alliance, both military and economic, between Russia and China. Right now the potential partnership between Russia and the European Union (EU) is dead with Russia turning definitively towards China. That was from the beginning the most likely outcome. Airbus never tried to establish a real partnership but rather a strategy to fade away the Russian aerospace industry. Actually Russia and China have formed a new alliance to build a long haul airliner. Western Europe (not to mention the United States) was never interested in the development of Russia or forming anything other than a master slave relationship with Russia providing raw materials and toeing the line of the West. It was clear then and today is a fact.

Russia has been preparing for a major war since 2008 and China has been increasing her military capabilities for the last 20 years. Today China is not a second tier power compared with the United States. Both in military and economic terms China is at the same level and in some specific areas are far ahead. In the domain of high-tech 5G has been a success in the commercial realm but the Type 055 destroyer is also another breakthrough with the US gaining a similar capability (DDG 51 Flight IIII) by mid of this decade (more likely by 2030). Nanchang, the lead ship of the Type 055 class, was commissioned amid the pandemic and lockdown in China.

Six years ago the likelihood of a major war was tiny. Since then it has grown steadily and dramatically and today is by far the most likely major event in the 2020s. The ultimate conflict can come from two ways. A conventional conflict involving at least two major powers that escalates into an open nuclear war. A second scenario is possible in the 2025-2030 timeframe. A Russian sneak first strike against the United States and its allies with the new S-500, strategic missile defenses, Yasen-M submarines, INF Zircon and Kalibr missiles and some new space asset playing the key role. The sneak first strike would involve all Russian missile strategic forces branches (bombers and ground-based missiles) at the different stages of such attack that would be strategic translation of what was seen in Syria in November 2015. There was no report that the Russian had such a capability of launching a high precision, multiple, combined arms attack at targets 2,000+ kilometers away. Western intelligence had no clue. The irony is that since the end of the Cold War the United States has been maneuvering through NATO to achieve a position to execute a first strike over Russia and now it seems that the first strike may occur but the country finished would be the United States.

Another particularity of the Western system is that its individuals have been brainwashed to the point that the majority accept their moral high ground and technological edge as a given. This has given the rise of the supremacy of the emotional arguments over the rational ones which are ignored or deprecated. That mindset can play a key role in the upcoming catastrophic events. At least in the Soviet system the silent majority of the people were aware of the fallacies they were fed up. We can see the United States claims about G5 being stolen from them by China or hypersonic technology being stolen by Russia as the evidence that the Western elites are also infected by that hubris. Over the next decade it will become obvious that the West is falling behind the Russia-China block and the malaise might grow into desperation. Going to war might seem a quick and easy solution to restore the lost hegemony to finally find them into a France 1940 moment. Back then France did not have nuclear weapons to turn a defeat into a victory. The West might try that swap because the unpleasant prospect of not being Mars and Venus but rather a bully and his dirty bitch running away in fear while the rest of the world is laughing at them.

If there is not a dramatic change of course the world is going to witness the first nuclear war. The Western block collapse may come before, during or after the war. It does not matter. A nuclear war is a game with billions of casualties and the collapse plays in the hundreds of millions.

UK, US, and Germany look to be “epicenters of slaughter”

Researcher Craig Paardekooper released this report on predictions of global population reduction from military analysis website Deagel.com.

Paardekooper’s article links mass slaughter to vaccines in countries inhabited mainly by White people of European descent.

Quote:

Deagel.com provided the forecast for population of each country. I obtained their forecast data before it was taken down in April of this year. However, the data had been safely archived and was still available for analysis.

I calculated the % population reductions for each country based on the difference between the current population and the forecast, and rank sorted each country in order of largest population reduction.

My hypothesis was that the cull would have an epicentre, centred in the countries/ powers who were running the pandemic – namely the G7.

I also hypothesised that those countries making the vaccines would right at the heart of the slaughter.

Observations

1. The G7 countries are clustered near the top of the list – their % population reductions are:

a. UK - 78.5%

b. USA - 70.2%

c. Germany - 65%

d. France - 41.8%

e. Italy - 30.6%

f. Canada - 29.7%

g. Japan - 17.6%

2. Three countries dominate the top positions:

a. UK

b. USA

c. Germany

These are the very 3 countries involved in the production of the vaccines: Astrazeneca, Moderna and Pfizer vaccines

If Deagel is an accurate forecast, then:

1. It is extremely dangerous to stay in UK, USA or Germany – the epicentres of this slaughter – the places where they make the vaccines (4 in 5 will die here).

2. G7 countries in general are a bad idea (1 in 3 will die at best).

3. European countries in general are unsafe.

4. The Eastern European countries appear to be the safer - Romania, Belize, Chechia, Lithuania, Finland, Hungry, Latvia.

5. There [is] quite a number of countries where there is no culling.

In Summary

It is advised that people temporarily distance themselves from UK, USA and Germany. These governments are planning the utter destruction of their own populations. And most are complying — it is almost like a suicide cult.

China comes in far down the list with just a 2.3% predicted reduction in population, from 1.390 billion to 1.358 billion people.

Population projections 2004-2050

EU25 population rises until 2025, then falls

Working age population expected to decrease by 52 million by 2050

Over the next two decades the total population of the EU25 is expected to increase by more than 13 million inhabitants, from 456.8 million on 1 January 2004 to 470.1 million on 1 January 2025 . Population growth in the EU25 until 2025 will be mainly due to net migration, since total deaths in the EU25 will outnumber total births from 2010. The effect of net migration will no longer outweigh the natural decrease after 2025, when the population will start to decline gradually. The population will reach 449.8 million on 1 January 2050 , that is a decrease of more than 20 million inhabitants compared to 2025 . Over the whole projection period the EU25 population will decrease by 1.5%, resulting from a 0.4% increase for the EU15 and a 11.7% decrease for the ten new Member States.

The share of the population of working age (between 15 and 64 ) in the total population is expected to decrease strongly in the EU25, from 67.2% in 2004 to 56.7% in 2050 , that is a fall of 5 2 million inhabitants of working age .

The share of the population aged between 0 and 14 will also be reduced , from 16.4% in 2004 to 13. 4% in 2050, while the proportion of elderly people (aged 65 and more) is expected to almost double over this period, from 16.4% in 2004 to 29.9% in 2050.

This information on population projections 1 in the EU25, Bulgaria and Romania, issued by Eurostat, the Statistical Office of the European Communities , has been derived from the analysis and extrapolation of demographic trends. Given the length of the projection period, results should be considered with caution.

Largest declines in most of the new Member States

In 2004 the population is estimated to have decreased in seven Member States ( the Czech Republic , Estonia, Latvia, Lithuania, Hungary, Poland and Slovakia). By 2025 the population will decrease in another six ; Italy (from 2013) , Germany and Slovenia (both 2014) , Portugal (2018), Greece (2020) and Spain ( 2022). By 2050, twenty Member States are expected to register a decline in their population; the previous thirteen plus Finland (from 2028), Austria (2029), Denmark (2032), the Netherlands (2036), Belgium (2037), the United Kingdom (2040) and France (2042). The population will still be increasing in Ireland, Cyprus, Luxembourg, Malta and Sweden.

Between 2004 and 2050 , the largest declines are expected to be observed in most of the new Member States : Latvia ( -19.2%), Estonia (-16.6%), Lithuania (-16.4%), the Czech Republic (-12.9%), Hungary and Slovakia (both -11.9%), and Poland ( -11.8%). Over the whole period, the strongest increases will be recorded in Luxembourg (+42.3%), Ireland (+36.0%), Cyprus (+33.5%) and Malta (+27.1%).

In absolute terms the largest population decreases are expected in Germany (-7.9 million), followed by Italy (-5.2 million) and Poland ( -4.5 million) , while the highest rises are expected in France (+ 5.8 million) , the United Kingdom (+4.7 million) and Ireland (+1.5 million).

Number of adults and young people down by 67 million by 2050

The proportion of the population in working age (between 15 and 64) is expected to decline sharply in the long run.

In the EU25 it will pass from 67.2% in 2004 to 56.7% in 2050, i.e. in absolute terms from 306.8 million in 2004 to 254.9 million in 2050. In 2050 the lowest shares of the population of working age will be observed in Spain (52.9%), Italy ( 53.5%), Portugal (55.0%) and Greece (55.2%) and t he highest in Luxembourg (61.3%), Malta (60.8%) and the Netherlands (60.7%).

The share of the EU25 population aged between 0 and 14 will decrease from 16.4% in 2004 to 13.4% in 2050. The largest decreases will be recorded in Cyprus (from 20.0% to 13.3%) and Ireland (from 20.9% to 16.0%). In 2050 the proportion of young people will range between 11.2% in Italy and 16.6% in Luxembourg.

More than 10% of the population aged 80 or over in 2050

On the other hand, the proportion of elderly people (aged 65 and more) is expected to rise substantially throughout the whole projection period. In the EU25 it will increase from 16.4% in 2004 to 29.9% in 2050, or from 75.3 million in 2004 to 134.5 million in 2050. The largest shares of elderly people in 2050 are expected in Spain (35.6%), Italy (35.3%), and Greece (32.5%), and the lowest in Luxembourg (22.1%), the Netherlands (23.5 %) and Denmark (24.1%).

The proportion of very o ld people (aged 80 and more) is expected to almost triple in the EU25, from 4.0% in 2004 to 11.4% in 2050, with the highest proportions expected in Italy (14.1%), Germany (13.6%) and Spain (12.8%).

As a consequence, the elderly dependency ratio 2 in the EU25 will rise from 24.5% in 2004 to 52.8% in 2050, while the young dependency ratio 3 would remain more or less constant throughout the projection period, passing from 24.4% in 2004 to 23.7% in 2050. The total dependency ratio 4 in the EU25 would increase from 48.9% in 2004 to 76.5% in 2050. This means that whereas in 2004 there was one inactive person ( young or elderly) for every two persons of working age, in 2050 there would be three inactive persons for every four of working age.

1. The Eurostat set of population projections is just one among several scenarios of population evolution based on assumptions of fertility, mortality and migration. The current trend scenario does not take into account any future measures that could influence demographic trends and comprises four variants: the ‘baseline’ variant presented in this News Release, as well as 'high population', 'low population' and 'zero -migration' variants, all available on the Eurostat website . It should be noted that the assumptions adopted by Eurostat may differ from those adopted by National Statistical Institutes (for example, assumptions about migration levels in Italy and Slovenia). Therefore, the results published by Eurostat can be different from those published by Member States.

2. Population aged 65 and more as a percentage of population aged between 15 and 64.

3. Population aged between 0 and 14 as a percentage of population aged between 15 and 64.

4. Sum of young and elderly dependency ratios.

5. Data for France refer to metropolitan France.

Issued by:

Eurostat Press Office:

Philippe BAUTIER

BECH Building

L-2920 Luxembourg

Tel: +352-4301-33 444

Fax: +352-4301-35 349

eurostat-pressoffice@cec.eu.int

Eurostat news releases on the Web:

http://europa.eu.int/comm/eurostat/

For further information:

Giampaolo LANZIERI

Fabio SARTORI

Konstantinos GIANNAKOURIS

Tel: +352-4301-35 336

Fax: +352-4301-36 049

giampaolo.lanzieri@cec.eu.int

fabio.sartori@cec.eu.int

konstantinos.giannakouris@cec.eu.int

Total population

Population at 1 January

(1000 inhabitants)

Percentage increase with

respect to 1.1.2004

2004 2015 2025 2050 2015 2025 2050

EU25 456 815 467 307 470 057 449 831 2.3 2.9 -1.5

EU15 382 674 394 727 398 780 384 356 3.1 4.2 0.4

New Member States 74 141 72 580 71 278 65 475 -2.1 -3.9 -11.7

Belgium 10 396 10 674 10 898 10 906 2.7 4.8 4.9

Czech Republic 10 212 10 012 9 812 8 894 -2.0 -3.9 -12.9

Denmark 5 398 5 498 5 557 5 430 1.9 2.9 0.6

Germany 82 532 82 864 82 108 74 642 0.4 -0.5 -9.6

Estonia 1 351 1 279 1 224 1 126 -5.3 -9.4 -16.6

Greece 11 041 11 390 11 394 10 632 3.2 3.2 -3.7

Spain 42 345 45 264 45 556 42 834 6.9 7.6 1.2

France5 59 901 62 616 64 392 65 704 4.5 7.5 9.7

Ireland 4 028 4 555 4 922 5 478 13.1 22.2 36.0

Italy 57 888 58 630 57 751 52 709 1.3 -0.2 -8.9

Cyprus 730 828 897 975 13.3 22.8 33.5

Latvia 2 319 2 174 2 068 1 873 -6.3 -10.8 -19.2

Lithuania 3 446 3 258 3 134 2 881 -5.5 -9.1 -16.4

Luxembourg 452 499 544 643 10.4 20.5 42.3

Hungary 10 117 9 834 9 588 8 915 -2.8 -5.2 -11.9

Malta 400 439 468 508 9.8 17.0 27.1

Netherlands 16 258 16 957 17 429 17 406 4.3 7.2 7.1

Austria 8 114 8 358 8 501 8 216 3.0 4.8 1.3

Poland 38 191 37 429 36 836 33 665 -2.0 -3.5 -11.8

Portugal 10 475 10 762 10 730 10 009 2.7 2.4 -4.4

Slovenia 1 996 2 019 2 014 1 901 1.1 0.9 -4.8

Slovakia 5 380 5 309 5 237 4 738 -1.3 -2.7 -11.9

Finland 5 220 5 354 5 439 5 217 2.6 4.2 -0.1

Sweden 8 976 9 373 9 769 10 202 4.4 8.8 13.7

United Kingdom 59 652 61 934 63 792 64 330 3.8 6.9 7.8

Bulgaria 7 801 7 130 6 465 5 094 -8.6 -17.1 -34.7

Romania 21 711 20 917 19 746 17 125 -3.7 -9.1 -21.1

Population structure – Main age groups

Percentage aged 0-14 Percentage aged 15-64 Percentage aged 65+

2004 2025 2050 2004 2025 2050 2004 2025 2050

EU25 16.4 14.4 13.4 67.2 63.0 56.7 16.4 22.6 29.9

EU15 16.3 14.4 13.5 66.7 62.8 56.5 17.0 22.8 30.0

New Member States 16.7 14.4 13.2 69.7 64.5 57.7 13.6 21.1 29.1

Belgium 17.3 15.6 14.7 65.6 61.9 57.6 17.1 22.5 27.7

Czech Republic 15.2 13.5 12.6 70.8 64.1 56.5 14.0 22.4 30.9

Denmark 18.9 15.9 15.7 66.2 62.9 60.2 14.9 21.2 24.1

Germany 14.7 12.9 11.9 67.3 62.5 56.5 18.0 24.6 31.6

Estonia 16.0 16.2 14.8 67.9 63.9 59.6 16.1 19.9 25.6

Greece 14.5 13.3 12.3 67.7 63.9 55.2 17.8 22.8 32.5

Spain 14.5 12.8 11.5 68.6 65.2 52.9 16.9 22.0 35.6

France5 18.6 16.7 15.8 65.1 60.9 57.0 16.3 22.4 27.2

Ireland 20.9 18.2 16.0 68.0 65.3 57.8 11.1 16.5 26.2

Italy 14.2 12.1 11.2 66.6 62.9 53.5 19.2 25.0 35.3

Cyprus 20.0 15.6 13.3 68.1 65.2 60.5 11.9 19.2 26.2

Latvia 15.4 16.2 14.8 68.4 64.1 59.1 16.2 19.7 26.1

Lithuania 17.7 15.1 13.7 67.3 65.7 59.6 15.0 19.2 26.7

Luxembourg 18.8 17.1 16.6 67.1 64.9 61.3 14.1 18.0 22.1

Hungary 15.9 14.3 13.8 68.6 63.7 58.1 15.5 22.0 28.1

Malta 18.2 15.6 14.5 68.7 63.1 60.8 13.1 21.3 24.7

Netherlands 18.5 16.1 15.8 67.6 63.3 60.7 13.9 20.6 23.5

Austria 16.3 13.8 12.3 68.2 64.1 57.3 15.5 22.1 30.4

Poland 17.2 14.6 13.0 69.8 64.3 57.6 13.0 21.1 29.4

Portugal 15.7 14.2 13.1 67.4 63.7 55.0 16.9 22.1 31.9

Slovenia 14.6 13.4 12.8 70.4 63.8 56.0 15.0 22.8 31.2

Slovakia 17.6 14.0 12.8 70.9 67.1 57.9 11.5 18.9 29.3

Finland 17.6 16.0 15.3 66.8 59.4 57.8 15.6 24.6 26.9

Sweden 17.8 17.1 16.3 65.0 60.7 59.4 17.2 22.2 24.3

United Kingdom 18.3 16.1 14.7 65.7 63.0 58.7 16.0 20.9 26.6

Bulgaria 14.2 11.7 11.5 68.7 64.5 55.0 17.1 23.8 33.5

Romania 16.4 14.1 12.5 69.1 66.9 57.9 14.5 19.0 29.6

Indicators of population structure

Young dependency ratio3 (%) Elderly dependency ratio2 (%) Total dependency ratio4 (%)

2004 2025 2050 2004 2025 2050 2004 2025 2050

EU25 24.4 22.9 23.7 24.5 35.7 52.8 48.9 58.7 76.5

EU15 24.5 23.0 23.9 25.5 36.3 53.2 50.0 59.3 77.1

New Member States 24.0 22.4 22.8 19.6 32.7 50.4 43.5 55.1 73.2

Belgium 26.4 25.2 25.4 26.1 36.5 48.1 52.5 61.7 73.5

Czech Republic 21.5 21.1 22.2 19.7 35.0 54.8 41.2 56.1 77.1

Denmark 28.5 25.3 26.0 22.5 33.8 40.0 51.0 59.1 66.0

Germany 21.9 20.7 21.1 26.8 39.3 55.8 48.7 60.0 76.9

Estonia 23.6 25.3 24.8 23.8 31.3 43.1 47.4 56.6 67.9

Greece 21.4 20.9 22.3 26.4 35.5 58.8 47.8 56.4 81.1

Spain 21.2 19.7 21.7 24.6 33.6 67.5 45.8 53.3 89.2

France5 28.5 27.4 27.7 25.2 36.9 47.9 53.7 64.3 75.6

Ireland 30.7 27.9 27.7 16.4 25.2 45.3 47.1 53.0 73.0

Italy 21.3 19.3 21.0 28.9 39.7 66.0 50.2 59.0 86.9

Cyprus 29.4 24.0 22.0 17.5 29.3 43.2 46.9 53.3 65.2

Latvia 22.5 25.2 25.0 23.6 30.7 44.1 46.1 55.9 69.1

Lithuania 26.2 23.1 23.0 22.3 29.2 44.9 48.6 52.2 67.8

Luxembourg 28.0 26.4 27.1 21.0 27.7 36.1 49.0 54.1 63.3

Hungary 23.1 22.4 23.7 22.6 34.5 48.3 45.7 56.9 72.0

Malta 26.5 24.7 23.9 19.0 33.8 40.6 45.5 58.4 64.6

Netherlands 27.4 25.4 26.1 20.5 32.5 38.6 47.9 57.9 64.7

Austria 23.9 21.5 21.5 22.8 34.5 53.2 46.7 56.0 74.6

Poland 24.7 22.6 22.6 18.6 32.8 51.0 43.3 55.4 73.5

Portugal 23.3 22.3 23.8 24.9 34.7 58.1 48.3 57.0 81.9

Slovenia 20.8 21.1 22.9 21.4 35.8 55.6 42.1 56.9 78.5

Slovakia 24.8 20.9 22.2 16.3 28.1 50.6 41.0 49.0 72.9

Finland 26.4 27.0 26.4 23.3 41.4 46.7 49.7 68.3 73.1

Sweden 27.4 28.2 27.5 26.4 36.5 40.9 53.8 64.6 68.4

United Kingdom 27.8 25.5 25.0 24.3 33.2 45.3 52.1 58.7 70.3

Bulgaria 20.6 18.1 21.0 24.9 36.9 60.9 45.5 55.0 81.9

Romania 23.8 21.0 21.6 20.9 28.5 51.1 44.6 49.5 72.6

The Deagel corporation is a minor branch of US military intelligence, one of the many secretive organizations which collects data for high-level decision-making purposes and prepares confidential briefing documents for agencies like the National Security Agency, the United Nations, and the World Bank. It is known, for example, to have contributed to a Stratfor report on North Korea. With this kind of pedigree, Deagel should be seen as a legitimate player in the intelligence community and not merely a disinformation asset. If so, then it must be assumed that its population predictions for 2025, as well as its industrial output predictions on a nation-by-nation basis, are based on strategic assumptions which are shared and well understood by other players in the intelligence community.

On 4/20/21, Deagel.com deleted their mysterious 2025 forecast spreadsheet that predicted a major collapse of the western countries but I have saved some archive links. The first one is interactive like it was when it existed on the Deagel website:

https://web.archive.org/web/20200629112402/http://www.deagel.com/country/forecast.aspx

https://www.thevoid.uk/void-post/deagel-2025-population-and-output-forecast-revisited-essential-guide/

PDF: https://www.ahava528.com/wp-content/uploads/2021/09/Deagel-Analysis-updated.pdf

As you can see from their current website this information is no longer there: https://deagel.com/

Info on the NWO/Great Reset: https://therealtruthnetworkcom.wordpress.com/2022/04/20/agenda-21-nwo/

Deagel Forecast

Country Pop. 2017 Pop. 2025 Pop. Change GDP Change ME Change PPP Change

United Kingdom 63,390,000 14,517,860 -77.1 -92.1 -97.7 -0.8

Ireland 4,770,000 1,318,740 -72.4 -88.9 -97.7 -0.7

United States of America 316,440,000 99,553,100 -68.5 -85.4 -95.6 -0.7

Puerto Rico 3,640,000 1,165,780 -68.0 -77.6 -0.3

Germany 80,590,000 28,134,920 -65.1 -83.0 -93.3 -0.7

Luxembourg 514,862 199,020 -61.3 -90.4 -97.8 -0.8

Israel 7,710,000 3,982,480 -48.3 -74.2 -89.3 -0.7

Libya 6,000,000 3,253,820 -45.8 -75.6 -0.7

Iceland 339,747 195,927 -42.3 -83.2 -96.0 -0.7

France 67,100,000 39,114,580 -41.7 -58.1 -81.5 -0.6

Spain 47,370,000 27,763,280 -41.4 -59.0 -81.8 -0.5

Bahrain 1,410,000 837,800 -40.6 -49.8 -75.9 -0.6

Cyprus 1,220,000 791,720 -35.1 -45.3 -57.9 -0.5

Australia 23,230,000 15,196,600 -34.6 -69.8 -90.1 -0.6

Angola 29,310,000 19,564,500 -33.2 10.8 13.4 -0.1

Switzerland 7,990,000 5,342,540 -33.1 -66.4 -84.8 -0.4

Denmark 5,600,000 3,771,760 -32.6 -56.3 -72.2 -0.5

Belgium 11,490,000 8,060,900 -29.8 -32.5 -55.2 -0.4

Austria 8,750,000 6,215,000 -29.0 -34.7 -61.2 -0.5

Ukraine 44,570,000 31,628,980 -29.0 -34.6 -50.3 -0.3

Italy 61,480,000 43,760,260 -28.8 -36.7 -63.0 -0.3

Malta 409,836 295,243 -28.0 -23.5 -54.4 -0.2

Syria 22,460,000 16,201,040 -27.9 -19.9 16.4 -0.3

Canada 35,620,000 26,315,760 -26.1 -35.9 -60.6 -0.5

Sweden 9,650,000 7,191,400 -25.5 -57.1 -78.8 -0.5

Estonia 1,250,000 932,320 -25.4 -14.4 -37.1 -0.3

Greece 10,770,000 8,055,960 -25.2 -39.4 -62.1 -0.4

Portugal 10,790,000 8,113,860 -24.8 -19.9 -43.9 -0.1

New Zealand 4,360,000 3,290,300 -24.5 -59.9 -83.2 -0.5

Country Pop. 2017 Pop. 2025 Pop. Change GDP Change ME Change PPP Change

Norway 5,080,000 3,833,960 -24.5 -66.3 -79.8 -0.5

South Korea 48,950,000 37,092,820 -24.2 -25.6 -59.2 -0.4

Moldova 3,620,000 2,750,860 -24.0 -2.5 -8.7 0.0

Lithuania 3,510,000 2,709,640 -22.8 10.3 36.4 0.2

Saint Lucia 162,781 127,192 -21.9 -5.7 -0.2

Barbados 292,336 229,598 -21.5 -22.1 -0.3

Taiwan 23,300,000 18,538,200 -20.4 -6.5 -29.1 -0.1

Latvia 2,180,000 1,755,520 -19.5 8.2 31.1 0.3

Japan 127,250,000 103,047,280 -19.0 -39.0 -63.7 -0.4

Belarus 9,550,000 7,863,440 -17.7 14.4 -28.8 -0.4

Serbia 7,240,000 5,966,200 -17.6 2.5 -39.6 0.0

New Caledonia 264,022 218,667 -17.2 -37.0 0.2

Bahamas 329,988 273,460 -17.1 -20.2 -0.3

Micronesia 106,104 89,473 -15.7 -81.2 -0.6

Uruguay 3,320,000 2,818,460 -15.1 -20.3 -59.2 -0.4

United Arab Emirates 5,470,000 4,664,700 -14.7 -52.2 -77.4 -0.1

Trinidad and Tobago 1,220,000 1,044,320 -14.4 -21.4 -21.1 -0.2

El Salvador 6,170,000 5,291,860 -14.2 7.6 9.2 -0.1

Bulgaria 7,100,000 6,128,360 -13.7 59.2 46.8 0.0

Qatar 2,040,000 1,764,240 -13.5 -54.0 -81.3 -0.5

Poland 38,380,000 33,230,780 -13.4 -18.4 -38.2 -0.1

Slovenia 1,990,000 1,723,800 -13.4 -7.5 -30.1 0.0

Croatia 4,290,000 3,754,250 -12.5 -7.4 -2.8 -0.2

Tanzania 48,260,000 42,526,920 -11.9 143.4 130.0 0.5

Equatorial Guinea 778,358 688,511 -11.5 16.9 -5.0 -0.4

Haiti 10,650,000 9,439,880 -11.4 18.5 -0.4

Turkey 80,690,000 71,556,440 -11.3 -4.9 -48.3 -0.2

Kuwait 2,690,000 2,401,080 -10.7 -43.8 -68.5 -0.2

Lesotho 1,940,000 1,749,080 -9.8 9.2 -22.9 -0.1

Burkina Faso 20,110,000 18,227,580 -9.4 113.7 143.8 0.2

North Macedonia 2,100,000 1,903,800 -9.3 67.8 67.2 -0.1

Country Pop. 2017 Pop. 2025 Pop. Change GDP Change ME Change PPP Change

Singapore 5,460,000 4,958,900 -9.2 -33.3 -58.8 -0.2

Montenegro 653,474 596,753 -8.7 74.3 45.2 0.6

Burundi 11,470,000 10,516,440 -8.3 104.3 106.7 0.2

Eswatini 1,470,000 1,358,340 -7.6 64.9 91.7 -0.3

Czechia 10,670,000 9,873,060 -7.5 0.8 0.5 -0.1

Slovakia 5,490,000 5,078,180 -7.5 6.6 0.3 0.2

Argentina 44,290,000 41,008,200 -7.4 -1.6 -27.4 -0.2

Aruba 115,120 107,067 -7.0 -1.6 0.1

Albania 3,050,000 2,840,580 -6.9 91.0 76.1 0.0

Bosnia and Herzegovina 3,860,000 3,613,500 -6.4 41.3 50.3 -0.1

Saudi Arabia 26,940,000 25,297,620 -6.1 -21.4 -35.6 0.0

South Africa 48,600,000 45,945,100 -5.5 -8.0 -42.8 -0.2

Armenia 3,050,000 2,891,200 -5.2 27.2 6.9 -0.2

Benin 11,040,000 10,493,240 -5.0 103.0 86.0 0.2

Jamaica 2,910,000 2,763,480 -5.0 9.5 -9.8 -0.2

Liberia 3,990,000 3,789,280 -5.0 10.3 -25.0 -0.1

World 7,226,458,211 6,871,665,908 -4.9 -15.9 -38.7 -0.2

Hungary 9,850,000 9,378,040 -4.8 37.2 15.1 0.0

Ecuador 16,290,000 15,519,180 -4.7 16.8 61.0 -0.1

Finland 5,520,000 5,268,640 -4.6 8.8 8.2 -0.1

Ethiopia 105,350,000 100,710,020 -4.4 109.4 150.7 0.1

Georgia 4,930,000 4,724,560 -4.2 68.7 67.3 -0.3

Guinea 12,410,000 11,896,000 -4.1 3.1 -34.9 -0.4

Suriname 566,846 543,830 -4.1 3.5 16.7 0.1

Thailand 67,500,000 64,978,140 -3.7 96.7 91.7 0.8

Romania 21,790,000 21,014,080 -3.6 84.4 85.0 0.7

Azerbaijan 9,960,000 9,630,860 -3.3 182.9 239.4 -0.1

Saint Vincent and the Grenadines 103,220 99,763 -3.3 34.5 0.1

Somalia 10,250,000 9,940,700 -3.0 150.4 -100.0 -0.3

Belize 360,346 351,422 -2.5 3.7 -19.0 -0.1

Cuba 11,150,000 10,871,820 -2.5 32.4 25.6 -0.1

Country Pop. 2017 Pop. 2025 Pop. Change GDP Change ME Change PPP Change

Fiji 920,938 899,721 -2.3 8.2 32.7 -0.2

Gambia 2,050,000 2,007,240 -2.1 76.1 0.0 -0.2

Cameroon 24,990,000 24,507,400 -1.9 116.7 92.6 0.1

Democratic Republic of Congo 83,300,000 81,698,120 -1.9 9.8 20.3 0.0

Brunei Darussalam 443,593 435,478 -1.8 88.3 39.4 0.0

Afghanistan 34,120,000 33,539,680 -1.7 448.9 3,284.5 1.6

Guyana 737,718 725,063 -1.7 22.7 3.9 0.0

Tunisia 10,830,000 10,644,240 -1.7 11.8 -15.6 -0.3

China 1,380,000,000 1,358,440,000 -1.6 42.1 37.0 0.1

Tonga 106,322 104,961 -1.3 30.8 -0.2

Grenada 111,724 110,668 -0.9 23.5 0.2

Russia 142,500,000 141,830,780 -0.5 104.9 98.3 1.4

Iran 82,020,000 81,976,680 -0.1 92.2 62.1 -0.3

Kiribati 103,248 103,179 -0.1 45.7 -0.5

Maldives 393,988 390,153 -1.0 98.9 28.6 0.7

Netherlands 16,800,000 16,809,740 0.1 7.2 -4.8 0.1

Brazil 207,350,000 210,314,920 1.4 35.2 36.9 0.0

Mali 15,970,000 16,208,120 1.5 146.7 228.7 1.2

Cape Verde 560,899 569,749 1.6 78.1 45.5 0.1

Chile 17,790,000 18,098,060 1.7 52.7 61.2 0.1

Djibouti 865,267 880,573 1.8 54.2 0.3

Ghana 27,500,000 27,991,840 1.8 54.7 44.5 -0.2

Eritrea 5,920,000 6,048,240 2.2 4.2 -0.3

Samoa 195,476 199,745 2.2 56.2 0.1

Kazakhstan 17,740,000 18,141,480 2.3 -1.7 -30.7 0.2

Botswana 2,210,000 2,262,280 2.4 52.9 11.9 -0.1

Indonesia 260,580,000 267,136,480 2.5 80.6 60.7 -0.2

Venezuela 28,460,000 29,243,520 2.8 -24.7 -55.8 -0.3

Chad 12,070,000 12,431,280 3.0 126.7 89.6 0.1

Colombia 47,700,000 49,240,520 3.2 83.7 74.5 0.1

Mauritius 1,320,000 1,363,960 3.3 40.9 36.4 0.1

Country Pop. 2017 Pop. 2025 Pop. Change GDP Change ME Change PPP Change

Morocco 32,650,000 33,767,920 3.4 99.7 90.7 0.6

Kyrgyzstan 5,550,000 5,753,600 3.7 36.8 229.0 0.0

Bhutan 758,288 787,650 3.9 78.6 -0.1

Malawi 16,770,000 17,488,020 4.3 162.5 76.5 -0.1

Sierra Leone 5,610,000 5,864,940 4.5 23.8 6.1 0.0

Costa Rica 4,930,000 5,154,640 4.6 14.3 -0.1

Dominican Republic 10,730,000 11,228,820 4.6 65.5 52.6 -0.1

Togo 7,150,000 7,477,160 4.6 126.4 136.8 0.7

India 1,280,000,000 1,341,720,000 4.8 110.0 85.7 -0.2

Uganda 34,760,000 36,458,240 4.9 112.0 111.6 0.3

Mexico 118,820,000 124,717,740 5.0 -1.1 -22.0 -0.1

Niger 16,900,000 17,764,280 5.1 125.0 376.6 0.7

Sri Lanka 21,670,000 22,791,540 5.2 159.1 133.1 0.6

Cote d'Ivoire 24,180,000 25,463,460 5.3 82.8 132.6 0.0

Iraq 31,860,000 33,754,520 5.9 62.3 240.4 1.1

Jordan 6,480,000 6,888,740 6.3 29.4 2.8 0.5

Myanmar 55,120,000 58,638,300 6.4 191.1 81.4 -0.2

Algeria 40,970,000 43,638,280 6.5 92.8 22.0 -0.3

Uzbekistan 28,660,000 30,541,480 6.6 108.8 78.7 0.4

Central African Republic 5,620,000 6,005,920 6.9 46.6 0.0

Peru 29,850,000 31,899,960 6.9 28.5 12.7 0.1

Rwanda 12,010,000 12,856,620 7.0 200.6 204.7 0.7

Nicaragua 5,790,000 6,202,240 7.1 71.9 47.9 0.0

Vietnam 92,470,000 99,030,160 7.1 175.7 177.0 0.7

Mongolia 2,910,000 3,118,360 7.2 91.5 50.8 0.7

Nigeria 174,510,000 187,254,300 7.3 142.7 91.2 0.9

Bolivia 11,140,000 11,981,200 7.6 52.0 41.4 -0.1

Gabon 1,770,000 1,904,720 7.6 100.8 78.0 0.1

Cambodia 16,200,000 17,454,060 7.7 119.5 113.6 0.0

Namibia 2,180,000 2,348,840 7.7 18.0 18.6 0.0

Zambia 14,220,000 15,322,840 7.8 39.2 17.2 0.6

Country Pop. 2017 Pop. 2025 Pop. Change GDP Change ME Change PPP Change

Mozambique 24,100,000 26,006,520 7.9 52.5 50.4 0.0

Panama 3,560,000 3,841,600 7.9 41.7 18.5 0.3

Senegal 13,300,000 14,384,940 8.2 101.0 144.1 0.5

Egypt 97,040,000 105,306,900 8.5 133.2 47.4 -0.2

Yemen 25,340,000 27,486,640 8.5 1.7 -23.6 -0.1

Turkmenistan 5,110,000 5,552,820 8.7 41.6 27.5 0.5

Honduras 9,040,000 9,840,640 8.9 30.1 -9.7 -0.2

Paraguay 6,620,000 7,238,960 9.3 43.9 31.6 0.3

Comoros 808,080 885,869 9.6 90.1 0.3

Guatemala 15,460,000 16,963,080 9.7 11.2 4.0 -0.2

Madagascar 22,590,000 24,842,620 10.0 88.1 47.2 0.1

Guinea-Bissau 1,790,000 1,979,800 10.6 95.7 104.5 0.0

Philippines 105,720,000 117,031,940 10.7 147.0 156.2 0.7

Solomon Islands 597,248 663,561 11.1 30.0 16.7 -0.2

Zimbabwe 13,180,000 14,638,960 11.1 45.9 4.9 1.5

Nepal 30,430,000 33,825,620 11.2 196.4 187.1 0.6

Mauritania 3,440,000 3,843,620 11.7 139.1 82.2 0.7

Malaysia 29,630,000 33,358,220 12.6 131.1 125.2 0.8

Bangladesh 157,830,000 178,356,440 13.0 58.5 24.1 -0.2

Pakistan 193,240,000 218,871,280 13.3 249.1 262.8 0.7

Vanuatu 261,565 298,136 14.0 61.6 -0.1

Kenya 44,040,000 50,320,160 14.3 179.5 141.5 1.0

Laos 6,690,000 7,665,700 14.6 210.5 106.5 0.9

Oman 3,150,000 3,616,920 14.8 2.0 5.7 0.1

Tajikistan 7,910,000 9,214,940 16.5 106.4 83.3 0.2

Timor-Leste 1,170,000 1,363,200 16.5 30.1 -1.7 -0.6

Republic of the Congo 4,570,000 5,330,360 16.6 86.6 382.9 0.5

Sudan 34,850,000 40,691,900 16.8 181.5 81.4 0.6

Papua New Guinea 6,430,000 7,571,120 17.7 44.6 41.4 0.1

Sao Tome and Principe 186,817 221,306 18.5 100.6 0.6

Lebanon 4,130,000 6,585,900 59.5 94.3 87.8 0.2

- Forecast For Iran And Most Of Middle East Forecast To Remain About Same

Over the past 9+ years and dating all the way back to October 22nd of 2014, ANP (All News Pipeline) has been reporting upon the absolutely bizarre 'forecast' for America and most of 'Western Civilization' being given by the 'US government sourced website' called the 'Deagel Report' for the near future, a 'forecast' which showed the United States population would be well below 100 million people soon and us looking economically and criminally like a 3rd world nation.

Called a 'crazy conspiracy theory' by the Associated Press and the mainstream media despite Deagel's sources being groups such as the US Department of Defense, the US Department of State, the CIA, the World Bank, the European Union and the US Navy, Army, Coast Guard, Marine Corp and Air Force, we've got to take another look at that forecast with us rapidly closing in on that 'End Date' as we barrel well into World War 3, and the fact that Deagel's forecast for the population of Israel also shows their population expected to be more than cut in half soon.

With Deagel forecasting at one point for the US's population to drop from 323 million+ to barely over 54 million soon as seen in this document at the website 'Pakistan Defense' from January 17th of 2018, a document called by them 'a cautionary tale highlighting weaknesses in our current systems,' take note that while the populations of Israel, the United States and most of Western Civilization are being forecast to tumble, the populations of nations such as Iran, Syria, Turkey as well as most of the Middle East were being forecast to largely stay the same or even increase.

Showing Israel's forecast to drop by a stunning 63.5%, that's nothing compared to the 79.7% forecast population drop for the United States of America, not to mention our forecast military expenditures are absolutely tumbling, as if we're seeing proof the 'US military industrial complex' from the year 2017 KNEW we were going to lose World War 3, and as a punishment by our 'future globalist rulers,' we were going to be 'disarmed' as a nation.

And as we had reported on ANP all the way back in 2014 when we first broke this bizarre forecast to our readers, Deagel also forecasted the United States would be a 3rd world nation soon economically, with our military spending being forecast to drop from $726 billion dollars yearly to only $8 billion dollars in the future, while our GDP per capita was forecast to drop from $52,838 to $13,328.

Also forecasting our gross domestic product to tumble to only $2.4 trillion soon, down from over $19 trillion in 2017, Deagel was largely blaming at the time a future devastating 'economic event' to be behind their forecast though as they also pointed out, global wars have long been drivers of such economic devastation through history.

ANP Emergency Fundraiser: The globalists war on ANP is all part of the globalists 'Big Tech' effort to silence conservative and independent voices, allowing them to maintain a monopoly on the flow of information. As George Orwell made clear to us decades ago, "The further a society drifts from the truth, the more they will hate those who speak it." But, with your amazing help, we at ANP promise to keep 'speaking truth to power' because, as Orwell also reminded us, "If liberty means anything at all it means the right to tell people what they do not want to hear."

With this new story over at The Express that Steve Quayle had linked to on his website earlier Tuesday morning reporting Russian President Vladimir Putin has turned against long time ally Israel, and that he now sees Israel 'as Russia's enemy,' being more proof of the World War 3 battle lines being drawn, take note that Deagel's forecast also saw the populations of both Russia and China staying largely the same, while that of 'Western Civilization' was decimated. Briefly, from this Express story before we continue.:

Vladimir Putin will now see Israel as an "enemy" as he moves closer to Iran and sides with Hamas in the Middle East, a former speechwriter for the Russian President tells Daily Express US.

Hamas has called Russia its “closest friend” as the terror group vows to release eight Russian hostages kidnapped during its October 7 attack in Israel.

Putin appears to be breaking from his previous line of neutrality over Israel and Palestine. This week he called on Israel to cancel its ground invasion into Gaza.

Abbas Gallyamov, a former speechwriter for Putin from 2008-2012 who lives in Tel Aviv, tells Daily Express US that Putin has become more reliant on Iran for weapons, and this is why he has shifted to a more pro-Palestine stance.

He said: "For many years Putin was really skillfully keeping a middle ground between Israel and Iran, but recently Russia became dependent on Tehran because of arms deliveries.

"He lost his chance to be an independent player. It was probably that Iran said 'we support you in Ukraine, you support us in the Middle East'.

"Putin had to follow Tehran. In the Middle East, Russia is quickly turning into another Iran proxy just like Hamas and Hezbollah."

The populations of the UK, the USA, Germany, Israel, France, Spain, Australia, Switzerland, Denmark, Belgium, Austria and numerous other countries were long being forecast to absolutely tumble. So what do the globalists who are behind the Deagel Report's absolutely bizarre forecasts for America and Israel know that the rest of us DON'T know?

December 28th of 2018 a story on ANP titled "If These Numbers From A Deep State Sourced Website Are Correct, America Will Be A 3rd World Nation - Deagel's Forecast Suggests The Depopulation End Game Has Arrived," providing us with Deagel's own explanation for why they were forecasting massive depopulation for Western Civilization.:

There have been many questions about the countries forecast specially the one focusing on the United States of America (USA). They won't be answered one by one but below you can find some explanation, thoughts and reflections. We are going to keep this as short as possible.

The majority of the economic and demographic data used in the making of the forecasts is widely available by institutions such as the CIA, IMF, UN, USG, etc.

The collapse of the Western financial system will wipe out the standard of living of its population while ending ponzi schemes such as the stock exchange and the pension funds. The population will be hit so badly by a full array of bubbles and ponzi schemes that the migration engine will start to work in reverse accelerating itself due to ripple effects thus leading to the demise of the States. This unseen situation for the States will develop itself in a cascade pattern with unprecedented and devastating effects for the economy.

Nevertheless the death toll will be horrible. Take into account that the Soviet Union's population was poorer than the Americans nowadays or even then. The ex-Soviets suffered during the following struggle in the 1990s with a significant death toll and the loss of national pride. Might we say "Twice the pride, double the fall"? Nope. The American standard of living is one of the highest, far more than double of the Soviets while having added a services economy that will be gone along with the financial system. When pensioners see their retirement disappear in front of their eyes and there are no servicing jobs you can imagine what is going to happen next. At least younger people can migrate. Never in human history were so many elders among the population. In past centuries people were lucky to get to their 30s or 40s. The American downfall is set to be far worse than the Soviet Union's one. A confluence of crisis with a devastating result.

And while the Deagel Report, soon after they published that explanation for why they were forecasting America to be a hugely depopulated, 3rd world nation soon, not only removed it but also removing their entire forecast, take note that they are still putting out military reports for countries all across the planet to this day, and their sources are still the same 'deep state' and globalists from years ago.

And as we'd reported in this July 21st of 2023 story on ANP titled "'Dystopian Fantasy' Coming True Before Our Eyes As Nobel Prize Winner's Dire Warning About 'Global Warming Hoax' Hints Of Massive 'Depopulation' As Warned Of In Deagel 2025 Forecast," we were watching America's collapse and destruction all across the country back then just a few months ago, and it's only getting worse as we move well into World War 3 though the mainstream media will never admit that.

With the destruction of America now easily seen in one big city after another, where mindless zombies are roaming around downtown areas, arms hanging low and no signs of life left what-so-ever in their faces or their spirits, we're already well on our way towards America being a 3rd world nation.

And with all of those cities being run by 'corrupt politicians' proving to us that they have no intention at all of truly HELPING 'people,' for if they did, they'd be spending money TRAINING them for jobs and careers rather than spending that money on free programs, it's not too difficult to see what this country will look like as a 3rd world nation.

Murders, street crime, white-collar crime, shoplifting, trespassing, abuse of power, illegal drugs, legal drugs, illegal immigration and open borders, election-tampering, institutional decay, homelessness, illiteracy, phony racism, real racism, corrupt politicians, vengeful district attorneys, child abuse, domestic partner abuse, disregard for human life, a weakened military, the rise of authoritarianism, expanding ignorance, AI, CRT, DIE, poverty, inflation, radical environmentalism, gender fluidity, lowered standards and weakened values, flight from personal responsibility, death of the meritocracy...the list goes on, and it's getting bigger by the day.

So with the Deagel Report over many years showing an absolutely bizarre 'forecast' for America, Israel and most of Western Civilization; the Deagel Report that composed those reports being 'sourced' by the 'deep state' here in America, including numerous United States government agencies; and those reports showing America, and Israel, completely 'depopulated' soon; and America and the world now only a little over one year away from that bizarre 'end times date,' we pray for everybody reading this, and Americans and people across the world, that God is with you, and gives each and every one of you, the strength and perseverance you'll need to make it through to the other side.

Deagel Makes Mysterious Changes To 2025 Population Forecast For America As Bill Gates Launches ‘Grand Challenge’.

The ‘Holy Grail Of Influenza Research’ And ‘Bridging The Valley Of Death’

While Microsoft founder and vaccine propagandist Bill Gates recently warned that the next deadly flu epidemic is just waiting around the corner and it could quickly lead to the deaths of more than 30 million people, we’re not the least bit surprised that he also claims a ‘universal flu shot’ is the answer to prevent such a deadly pandemic, this despite the fact that even medical experts claimed that this year’s flu shot was hardly a preventive and actually led to the spread of the flu.

With the Bill and Melinda Gates Foundation teaming up with Google co-founder Larry Page to launch the ‘Grand Challenge’ of what they call the ‘holy grail of influenza research‘, an attempt to develop a ‘universal vaccine‘, Gates and Page are giving out individual grants of between $250,000 and $2 million over 2 years to those attempting to develop such a universal flu shot with human testing set to begin by 2021.

Calling upon computational biology, bioinformatics, artificial intelligence, machine learning and other new technologies to be used as aids in the ongoing research, Gates and Page hope to ‘bridge the funding‘ of such projects due to what they call the “valley of death” between novel concepts and clinical trial-ready products.

And while like many globalists, Gates and Page sound ‘sincere’ in their goals to prevent the spread of an epidemic that could cull tens of millions of lives, we must always remember that Gates and the Gates Foundation are also proponents of eugenics with Gates himself coming out directly and stated the world is far too overpopulated, while his father, William H Gates Sr., was a former board member of ‘Planned Parenthood’.

Bill Gates has doubled down on his goal to depopulate the planet, using deceitful Orwellian doublespeak in a new video to bamboozle his naive followers into believing that “by making people healthier, we can reduce the world’s population”.

Make no mistake, when Gates talks about “making people healthier” what he is really talking about is enforcing the mandatory roll out of his range of experimental vaccinations. The same vaccines that have already caused mass sterilization and death on multiple continents.

The second-richest man on the planet is a committed globalist and eugenicist working towards the New World Order goal of depopulation. Lest anyone forget these facts, Bill Gates regularly goes out of his way to remind us of them.

Bill Gates and his foundation have consistently come under fire for their goal of depopulation, and now the same man who admitted in a TED talk that his goal is to eliminate a billion humans from the face of the Earth has now taken to Facebook to lecture us about why being eradicated is in our own interests.

And while the website Deagel.com has recently made some very mysterious changes to their 2025 forecast for America as we report in much more detail below, as we hear in the video from the Leak Project and read in a March story from The Sun, one medical health expert is warning of a mutant virus that sounds straight from a science fiction movie, potential becoming the fastest-spreading viral killer known to the human race and as he tells us, such a killer virus outbreak could happen tomorrow.

Dr Jonathan Quick, chair of the Global Health Council, said the flu virus is “the most diabolical, hardest-to-control, and fastest-spreading potential viral killer known to humankind”.

Describing what sounds like scenes from a horror film, Dr Quick warned in The Daily Mail of starvation, medicine supplies running low, energy systems crippling under the pressure and the collapse of the global economy.

And what’s could cause such devastation, on a global scale?

“The most likely culprit will be a new and unprecedentedly deadly mutation of the influenza virus. The conditions are right, it could happen tomorrow.”

And while the website Deagel.com is STILL forecasting a massive depopulation for America, on our visit to their website recently we found a huge difference in their forecast.

As we had reported on ANP back on December 31st of 2017, Deagel was previously forecasting the US population to drop to 54 million people soon, down from what was then 324 million people in 2016. Deagel is now forecasting that the future population of the USA will be a nice, round 100 million people – nearly doubling their previous forecast for America of 54 million.

Yet as it’s easy to see, even a forecast of 100 million people living here in less than 8 years is STILL DOWN 227 million from the 2017 population of America. How will America LOSE 227 million people?

We’d love to know why Deagel is forecasting the population of the US to drop from 327 million in 2017 to only 100 million, with them also forecasting a US military budget of 32 billion dollars, down from our 2017 military budget of $637 billion, while forecasting our population density to drop from 34 inhabitants per square mile to only 10 inhabitants per square mile in the near future. What does Deagel know that we don’t know?

Also forecasting that our gross domestic product will drop from $19 trillion in 2017 to only $2.4 trillion soon, Deagel’s numbers for America still show an America in total collapse, a 3rd world nation with our GDP per capita more than cut in half while our purchase power parity is forecast to be lower than Thailand, Columbia, Bulgaria, Croatia and Montenegro.

And before you go and discount Deagel’s numbers, its very important to know that their sources ARE the ‘deep state’ with the CIA, US Department of Defense, US Department of State and World Bank contributing data for their forecasts. So…. what does Deagel know what we don’t know? Their sources make clear that whatever Deagel knows, the ‘deep state’ knows, too!

While Deagel leaves no explanation on their website about why they’ve made these changes to their forecast population of America, as we’ve previously reported, they did put out an explanation back in October of 2014 about why they were forecasting such a huge drop for America, ‘a confluence of crisis’ with a devastating result‘. A brief excerpt from that 2014 explanation:

The key element to understand the process that the USA will enter in the upcoming decade is migration. In the past, specially in the 20th century, the key factor that allowed the USA to rise to its colossus status was immigration with the benefits of a demographic expansion supporting the credit expansion and the brain drain from the rest of the world benefiting the States.

The collapse of the Western financial system will wipe out the standard of living of its population while ending ponzi schemes such as the stock exchange and the pension funds. The population will be hit so badly by a full array of bubbles and ponzi schemes that the migration engine will start to work in reverse accelerating itself due to ripple effects thus leading to the demise of the States. This unseen situation for the States will develop itself in a cascade pattern with unprecedented and devastating effects for the economy. Jobs offshoring will surely end with many American Corporations relocating overseas thus becoming foreign Corporations!!!!

We see a significant part of the American population migrating to Latin America and Asia while migration to Europe – suffering a similar illness – won’t be relevant. Nevertheless the death toll will be horrible. Take into account that the Soviet Union’s population was poorer than the Americans nowadays or even then. The ex-Soviets suffered during the following struggle in the 1990s with a significant death toll and the loss of national pride. Might we say “Twice the pride, double the fall”? Nope.

The American standard of living is one of the highest, far more than double of the Soviets while having a services economy that will be gone with the financial system. When pensioners see their retirement disappear in front of their eyes and there are no servicing jobs you can imagine what is going to happen next. At least younger people can migrate. Never in human history were so many elders among the population. In past centuries people were lucky to get to their 30s or 40s. The American downfall is set to be far worse than the Soviet Union’s one. A confluence of crisis with a devastating result.

And while their expected culling of 227 million Americans isn’t quite as many as they were forecasting just weeks ago, they are still forecasting a huge drop for America’s population within less than 8 years, a population drop-off which is still unadequately explained, even using their 2014 explanation seen in the previous section of this story above.

While the mainstream media and gatekeepers such as snopes will continue to call the globalists depopulation agenda a ‘conspiracy theory’ despite the fact that its written in granite upon the mysterious Georgia Guidestones that were recently blown up and now removed, we hear from videographer Truth Happens about Gates plans for a universal vaccine with our videographer also talking with us about the globalists depopulation agenda.

And in the final video from videographer ‘Leak Project’ about the suspect ‘mutant virus’ on the loose that some warn could eventually lead to the deaths of 300 million or more, with medical experts warning the conditions for such a deadly outbreak are perfect despite the fact that they still don’t even know exactly what will cause this ‘outbreak’.

BILL GATES CONTRIBUTIONS TO VACCINES:

Bill Gates, the Microsoft founder turned philanthropist has spent billions to help bring vaccines to the developing world, working closely with pharmaceutical executives to transform the market. In doing so, he has become one of the more powerful — and provocative — private player in global health.

THE PAST:

The GAVI Alliance celebrated the tenth anniversary of its foundation on Jan 29 this year 2010. During its 10 years GAVI has overseen the delivery of vaccines to around 250 million children in the world's poorest countries.

To mark GAVI's birthday, the Bill and Melinda Gates Foundation announced that it will commit US$10 billion over the next 10 years to a so-called decade of vaccines—ie, research and development and delivery of vaccines to the world's poorest. As an agency whose role is vaccine delivery, rather than research and development, it is not clear how much of the Gates billions will be coming to GAVI. However, GAVI is already the foundation's largest grantee, having received $1·5 billion in its 10 year history.

Other major GAVI donors are national governments, of which 16 have contributed to the alliance plus the European Commission. Countries that have donated the most to GAVI's core funding include Canada, the Netherlands, Norway, the UK, and the USA. Although the direct donation made by Gates far outstrip those made by any national government, France and the UK have committed billions of dollars to a funding mechanism called the International Finance Facility for Immunization and other governments have promised substantial amounts to this scheme.

GAVI currently disburses around $1 billion per year among the 65 countries in which it supports vaccination programmes. The alliance focuses its activities on delivery of a childhood pentavalent vaccine that protects against diphtheria, tetanus, pertussis, hepatitis B, and Haemophilus influenzae type b. However, to roll out this vaccine to all 65 countries by 2015, plus achieve its goal of adding pneumococcal and rotavirus vaccines to the immunisation schedule, will require an additional $3 billion.

A lot more than just wishful thinking has gone into Gates' decision to donate $10 billion. A model developed at the Johns Hopkins Bloomberg School of Public Health (Baltimore, MD, USA), indicated that 90% vaccine coverage—including the rotavirus and pneumococcal vaccines—would prevent the deaths of 7·6 million children younger than 5 years between now and 2020. Adding the malaria vaccine, which is undergoing clinical trials, from 2014 could save an additional 1·1 million lives. The Gates Foundation will certainly not be funding this expansion in vaccine coverage on its own, but its financial commitment should act as an incentive for donor governments to provide the additional funds to achieve 90% coverage with childhood vaccines in developing countries within the next 10 years.

In addition to the diseases already mentioned, vaccination against measles will likely be targeted for some of the Gates' billions. Progress in preventing deaths from measles has been remarkable, with around 82% of those eligible worldwide now receiving vaccine and the number of measles-related deaths falling from around 750 000 in 2000 to 164 000 in 2008. GAVI does not currently fund measles vaccination programmes; rather, another international collaboration, the Measles Initiative, provides technical and financial support for national vaccination programmes in developing countries. Other areas that might benefit include the provision of autodisposable syringes that cannot be reused, funding for new vaccines against group A meningococcal meningitis and against tuberculosis, and perhaps even a final push to eliminate polio.